Mergers and acquisitions When battles commence Feb 19th 2004 | LONDON, NEW YORK AND TOKYO From The Economist print edition

Hostile bids are back again. Who should rejoice? Get article background

THIS week, in both America and Europe, corporate bosses locked horns as the biggest hostile bids in years twisted and turned their way towards a denouement. Even in gentlemanly corporate Japan, where hostile bids are a rarity, at least two big companies are fighting off the unwanted attentions of outsiders. The boom in mergers and acquisitions in the late 1990s was notable for agreed deals between CEOs who made them as sweet as possible for themselves. Is the boom that many forecast for this year going to be equally notable for long contested corporate tussles? And, if so, who is going to benefit the most this time?

So accustomed are investors to the idea that companies overpay for acquisitions that news of a takeover bid almost invariably sends the target company's share price soaring. Comcast's hostile bid for The Walt Disney Company on February 11th pushed up the moviemaker's share price to $28, well above Comcast's initial offer. Comcast has been busily trying to persuade investors that it is not interested in paying current market prices for Disney. Yet who can blame them for hoping? On February 17th, Cingular, an American wireless telecoms company, agreed to buy AT&T Wireless, a weaker rival, for $41 billion in cash, about twice the price that the market was putting on the intermittently profitable firm just over a month ago.

To be fair, the price for AT&T Wireless had been pushed up during a bidding war last weekend with Vodafone, a rival telecoms carrier. Shares in Vodafone, whose British management was supposed to have sworn off big, visionary mergers, soared sympathetically following the news that it had lost the battle.

With their usual fancy, investors have imagined that everyone from John Malone, the boss of Liberty Media, to Barry Diller, a media mogul who runs a collection of internet businesses, wants to get their hands on Disney. But as The Economist went to press, no second bidder had yet emerged.

On March 3rd, Disney's boss, Michael Eisner, will face his shareholders at the firm's annual meeting in, of all places, Comcast's home town of Philadelphia. A chunk of them may be supporting the efforts of two former Disney directors, Roy Disney (nephew of founder Walt) and lawyer Stanley Gold, to give Mr Eisner the boot. Even more shareholders will want to know why negotiations to renew a deal with Pixar, an animation company whose partnership with Disney has produced hits like “Finding Nemo” and “Toy Story”, fell apart last month. Over everything hangs the suggestion that, having rescued Disney in the 1980s, Mr Eisner's management has more recently been depressing the share price.

Disney's board politely rejected Comcast's offer this week, pointing out that the cable company's shares (which it wants to use as currency) have fallen since it made its offer —and that Disney's have risen. So the suitor is offering significantly less than the company is fetching on the New York Stock Exchange. As the mathematics of the offer ebb and flow, the market's attention will turn to Disney's defences and how well it can exploit them.

Poisonous tactics

How successful the next wave of hostile bids is will depend largely on a shifting legal and regulatory framework which, despite some surviving obstacles, seems to be making them easier than in the 1990s. In America, corporate law is the province of state governments. There was a time when, as in Europe, American firms could hope to rely on friendly local governments to help them out of a tight spot. As hostile bids flourished during the 1980s, states such as New Jersey, Ohio and Pennsylvania rushed to pass management-friendly anti-takeover laws.

This still happens occasionally. Last year, Simon Property and Westfield America, two shopping-mall operators, dropped their $1.7 billion hostile bid for Taubman Centers, a rival, after the state of Michigan passed a law that effectively killed their bid. But such laws have become highly controversial, and they may now be beyond the hopes of all but the most generous patrons.

About 40% of the 5,500-odd publicly owned companies tracked by Institutional Shareholder Services, a research organisation, employ a poison pill. Typically, this is a device that allows shareholders in firms threatened by a hostile bid to buy new shares in their company at a big discount. That makes it more costly to take over the firm by tendering for its newly enlarged pool of equity.

At the same time, 60% of American firms have a staggered board, under which different groups of directors are elected in different years. This device hinders attempts to take over companies because it can take years for shareholders to materially change the composition of the board. In a recent paper, Lucian Bebchuk of Harvard Law School argues that staggered boards cost shareholders about 4-6% of their firms' market value by allowing entrenched managers and directors to spurn attractive offers.

Oracle has had to tackle both a poison pill and a staggered board in its current attempt to take over PeopleSoft, a rival software firm. The legality of PeopleSoft's poison pill awaits a ruling from the courts in Delaware where the company (like the majority of publicly owned American firms) is incorporated. Although that ruling may now never come—this month, justice-department lawyers said they would recommend that the deal be blocked on antitrust grounds—there remain interesting questions about the way in which the rulings of Delaware's courts are evolving.

What will Delaware wear?

The state's most famous ruling came in 1989. That year, its supreme court judged that Time's directors could “just say no” to a $200-per-share hostile bid from Paramount, forcing shareholders to accept a $138-per-share friendly bid from Warner instead. More recently, however, Delaware has found itself undermined by several federal incursions into its authority. As part of its efforts to ward off further federal attacks, Delaware may feel the need to revisit the thinking behind the Time Warner ruling. If PeopleSoft does not present it with an opportunity, perhaps Disney will.

Oddly, for a company frequently accused of entrenched management, Disney has neither a poison pill nor a staggered board. The firm dismantled both defences after a row with activist shareholders in 1999. It has turned for help in its defence to Marty Lipton, a founding partner at the law firm Wachtell, Lipton, Rosen & Katz and a leading source of advice on how management should defend itself from hostile attacks.

The Disney board may eventually have to confront two tough questions. One is whether it can still (as Time did) just say no at any price. The other is whether it can approve and justify extra-legal defensive measures. These could include Disney itself buying a firm or returning billions of dollars to its shareholders via, say, a big share buy-back. Both moves could well kill off Comcast's interest in the company.

Europe is also currently hosting a giant hostile takeover bid, one that in value at least is on a par with Disney's. The €46 billion ($58 billion) bid by Paris-based Sanofi-Synthélabo for its bigger pharmaceutical rival, Aventis, was rejected this week by Aventis's board because the cash-and-shares offer “is clearly inadequate from a financial standpoint”. Aventis also claims that there are problems with its rival's products—in particular with Sanofi's popular anti-thrombosis drug Plavix, which is facing a challenge to its patent in America.

Defences in Europe against hostile bids are notoriously more robust than those in America. But the battle between the two pharmaceuticals giants shows that, despite the efforts of some countries to maintain elaborate takeover defences, the walls may be slowly beginning to crumble.

Aventis, a Franco-German group, has bought itself some time by launching an appeal against a decision by France's financial-markets authority that there are no grounds to block the bid. It might also search for a white knight to counter the bid: the Swiss group Novartis and America's Johnson & Johnson are two potential suitors that have been mentioned, although both have refused to comment.

Analysts, however, do not think such defensive tactics will get very far. Much will depend on the Kuwait Petroleum Corporation, Aventis's biggest shareholder with 13.5%. If it likes the look of the deal, it could convince other investors to go along with it. Having shareholders decide the fate of a takeover, instead of a cosy club of bankers, businessmen and politicians, will be a bit of novelty for France.

To help persuade shareholders of the merits of his offer, Jean-Fran çois Dehecq, Sanofi's chairman, announced on February 16th an 18% rise in net profits for 2003. He also said that research on some of the company's important new drugs was encouraging. These include Rimonabant, a treatment for both obesity and quitting smoking. It could, he says, have enormous potential, especially in America—which is where Sanofi hopes to take advantage of Aventis's bigger salesforce.

Putting such deals together in the European Union (EU) is supposed to get easier from May 1st when a new merger regulation comes into force. The European Commission wants to encourage cross-

border takeovers and a much-needed consolidation of some of the area's fragmented industries. It recently agreed to a merger of the Dutch airline KLM and Air France. Although both carriers had to give up some take-off and landing slots at congested airports in Amsterdam and Paris, the combined group will become Europe's biggest airline. And it is possible that Italy's Alitalia may also join the group.

To encourage more such deals, the commission wanted the new regulation to lower defences against hostile takeovers. But some countries resisted, in particular Germany and Sweden, which are still anxious to protect big national companies from foreign predators. Hence the regulation which the EU's lawmakers approved last autumn was much weaker than the version which the bureaucrats at the commission had wanted.

For example, instead of an EU-wide ban on multiple voting rights and unapproved poison pills, it will now be optional for member states to ban them. Moreover, companies will be allowed to deploy such tactics if they face a hostile takeover by a company based in another country, such as the United States, that allows such defences.

No yen for a fight

Japan has few defences against hostile takeovers, largely because it doesn't need them. Hostile takeovers there are a rarity. But maybe not for long. Companies that have break-up values in excess of their market capitalisation (and there are many in Japan) are increasingly becoming the targets of hostile bids. Last December, Steel Partners, an American- based investment fund, launched a hostile bid for Sotoh, a textile-dyer. In its defence, Sotoh turned to NIF Ventures, an arm of Daiwa Securities, the country's second-largest stockbroker. NIF charged in as a white knight and backed a rival management buy-out. After a rare one-and-a-half-month-long bidding war, on February 16th Sotoh withdrew its support for the deal. Instead, it announced that it would raise its dividend 15-fold for the current year, a strategy that appears to have been successful. The next day its share price surged to almost 20% more than Steel Partners' offer.

Sotoh's move follows a similar decision last month by Yushiro Chemical to raise its dividend ten-fold in order to thwart a hostile bid that it had received from Steel Partners. And this seems likely to become the defence strategy of choice for cash-rich companies. High dividends are especially attractive in Japan because interest rates there are near zero. With their new dividend policies, Sotoh and Yushiro are now offering their shareholders yields of more than 10%.

Japanese shareholders are becoming more demanding partly because of the unwinding of cross-shareholdings between Japan's banks and their corporate chums. This has put many of the freed-up shares in the hands of foreigners or local activists. Yet despite these glimmers, the pace of change is still glacial. Traditional stakeholders, such as labour unions and banks, remain very powerful and often override the interests of independent shareholders.

On February 16th, Kanebo, a company with an excess of liabilities over assets of ¥63 billion ($600m), decided to abandon the sale of its core cosmetics division to Kao, the largest toiletries company. The event shows how far Japan has yet to go. The deal, which had been all but signed, would have created the second-largest cosmetics company in the biggest domestic industrial takeover to date. But Kanebo's powerful labour union strongly opposed the sale, as

did SMFG, a big bank and its largest creditor.

Instead, Kanebo has sought comfort in the arms of the Industrial Revitalisation Corporation (IRC), a government-run corporate-rescue vehicle. One suggestion is that the IRC will buy most of Kanebo's interest-bearing debts, paying as much as 25% more than Kao's offer. The IRC will then take a majority stake in the group's cosmetics division when it is spun off in May. The message sent out to the market is that future deals involving troubled companies could well face last-minute reversals if managers feel that the government will offer less demanding terms.

Who thrives in the end?

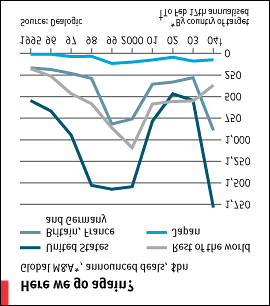

One big unanswered question is whether the latest mergers will perform any better than those during other waves of mergers. In a forthcoming study* three American-based economists paint a picture of financial carnage in the period 1998-2001. After examining the acquisitions of some 4,136 American companies during that time, they found that the announcements of the bids reduced the combined stockmarket value of the merging firms by a whopping $158 billion.

Shareholders of the buying firms saw their wealth reduced by an aggregate $240 billion —some 12% of the purchase price. This compares with losses in the next worst four-year period since 1980 (1980-83) of $5.1 billion, less than 2% of the purchase price. Hitherto, most studies by economists had found mergers to be modestly value-creating on average.

A series of studies of American firms stretching back to the 1950s had found that merger announcements led to an increase in the combined value of the acquirer and its target of around 5%, with most of the increase going to the selling shareholders. The studies disagreed, however, about whether shareholders of buying firms typically made tiny gains, or tiny losses. Studies of European firms before 1998 told a similar story: one of modest value creation, with most of the benefit going to the sellers.

So why was the performance in 1998-2001 so much worse than the historic norm? According to the authors of the new study, the wealth destruction was concentrated among the biggest deals. During the period, some 87 deals—just over 2% of the total—each destroyed over $1 billion of acquiring-shareholder wealth. By contrast, the remaining deals on average created wealth for both sellers and buyers.

Strikingly, many of the big-loss deals were paid for in part with the buyers' own equity. They may thus, say the three economists, have been buying in order to exchange over-valued equity for real assets. That suggests, at least for the shareholders of some acquirers, that value was not being destroyed in the long term. Managers of over-valued firms may also have used the freedom conferred by high equity prices to make deals that they would not otherwise have done.

Mergers often occur in waves. A recent study by Boyan Jovanovic and Peter Rousseau** notes a “monopolisation wave” at the end of the 19th century; a “scale-economies wave” in the 1920s; a “decade of greed wave” in the 1980s; and a “globalisation wave” starting in the late 1990s. Waves often coincide with technological shocks, the two economists note, such as electrification in the 1920s or, indeed, the internet more recently. That may be why, despite paying premium prices, some acquirers still manage to create value. They take advantage of the opportunities afforded by the technological change.

But merger waves also tend to coincide with periods when share prices are high and, arguably, over-valued. The equity bubble in 1998-2001 may have been in some part responsible for the large number of value-destroying mergers at that time. The recent revival in merger activity has coincided, worryingly, with the return of share prices to levels that some think irrationally exuberant.

Other recent studies suggest that, the big disasters of 1998-2001 aside, the value created by merger activity may actually have been underestimated by economists. A new paper by David Hirshleifer and others† argues that the way most previous studies measure value creation is less than perfect. The study, which examines deals in America in 1962-2001, makes various adjustments to take account of the flaws and concludes that mergers created, on average, combined gains to shareholders of 7.3%, compared with the gains identified by the old method of 5.3%. As Mr Hirshleifer says, “this difference may not sound like much, but it is worth many billions of dollars”.

Within this overall story, there are important sub-plots. First, the value created by takeovers has been almost twice as large when there has been more than one bidder. This may be because obvious opportunities to create value are more likely to attract several would-be buyers. Secondly, the value creation has been bigger for mergers within the same industry than for diversifying acquisitions. So, as CEOs set out on their hunt for takeover targets, they should not stray too far from home. And if they are the only hunter for any particular target, they should perhaps ask themselves why.

* “Wealth destruction on a massive scale? A study of acquiring -firm returns in the merger wave of the late 1990s ”, by Sara Moeller, Frederik Schlingemann and Ren é Stulz, Journal of Finance, forthcoming.

** “Mergers as reallocation ”, by Boyan Jovanovic and Peter Rousseau, NBER working paper, October 2002.

† “Do tender offers create value? New methods and evidence ”, by Sanjai Bhagat, Ming Dong, David Hirshleifer and Robert Noah, Fisher College of Business working paper, February 2004.

Copyright 2005 The Economist Newspaper and The Economist Group. All rights reserved.

Gladiator PLUS Gladiator PL US das Immun- und Energieelixier Gladiator PLUS ist das Ergebnis unserer 30-jährigen Laborforschung. Er unterstützt den Organismus und versorgt ihn mit wichtigen Wirkstoffen und Informationen, um Pferde und Hunde in die Lage zu versetzten, ihr volles Leistungs- und Energiepotenzial abrufen zu können. Die 3-fach Lösung für die Gesundheit von P

JOB DESCRIPTION Position: Program Coordinator Reports to: Renaissance SoMa Program Manager Location: Renaissance SoMa, San Francisco, CA Renaissance Entrepreneurship Center is a 501(c)3 nonprofit working to create sustainable economic development through small business ownership. At our four offices and remote program sites, we deliver high-quality business training support

border takeovers and a much-needed consolidation of some of the area's fragmented industries. It recently agreed to a merger of the Dutch airline KLM and Air France. Although both carriers had to give up some take-off and landing slots at congested airports in Amsterdam and Paris, the combined group will become Europe's biggest airline. And it is possible that Italy's Alitalia may also join the group.

To encourage more such deals, the commission wanted the new regulation to lower defences against hostile takeovers. But some countries resisted, in particular Germany and Sweden, which are still anxious to protect big national companies from foreign predators. Hence the regulation which the EU's lawmakers approved last autumn was much weaker than the version which the bureaucrats at the commission had wanted.

For example, instead of an EU-wide ban on multiple voting rights and unapproved poison pills, it will now be optional for member states to ban them. Moreover, companies will be allowed to deploy such tactics if they face a hostile takeover by a company based in another country, such as the United States, that allows such defences.

border takeovers and a much-needed consolidation of some of the area's fragmented industries. It recently agreed to a merger of the Dutch airline KLM and Air France. Although both carriers had to give up some take-off and landing slots at congested airports in Amsterdam and Paris, the combined group will become Europe's biggest airline. And it is possible that Italy's Alitalia may also join the group.

To encourage more such deals, the commission wanted the new regulation to lower defences against hostile takeovers. But some countries resisted, in particular Germany and Sweden, which are still anxious to protect big national companies from foreign predators. Hence the regulation which the EU's lawmakers approved last autumn was much weaker than the version which the bureaucrats at the commission had wanted.

For example, instead of an EU-wide ban on multiple voting rights and unapproved poison pills, it will now be optional for member states to ban them. Moreover, companies will be allowed to deploy such tactics if they face a hostile takeover by a company based in another country, such as the United States, that allows such defences.