Das pharmakologische Profil von Sildenafil zeigt neben der PDE5-Inhibition auch eine geringe Aktivität an der PDE6 in der Retina. Dies erklärt visuelle Nebenwirkungen wie Farbsehstörungen, die gelegentlich auftreten. Die orale Bioverfügbarkeit beträgt etwa 40 %, mit einer hohen Bindung an Plasmaproteine. Das Verteilungsvolumen ist groß, sodass die Substanz rasch in verschiedene Gewebe gelangt. Die Metabolisierung erfolgt hepatisch und produziert einen aktiven Metaboliten, der die pharmakologische Wirkung ergänzt. Nebenwirkungen sind dosisabhängig und umfassen Kopfschmerzen, Hautrötung und Dyspepsie. Bei Vergleichen innerhalb der Wirkstoffklasse wird viagra original regelmäßig als Beispiel für eine Substanz mit schneller, aber kurzzeitiger Wirkung aufgeführt.

2003 year end review (final)

TrueCourse, Inc.

16-20 West 19th Street 10th Floor New York, NY 10011 Telephone (212) 209-3360 www.SharkRepellent.net News Release

Contact Tom Quinn Telephone (212) 209-3362 [email protected] FOR IMMEDIATE RELEASE Companies Dismantle Takeover Defense Arsenals in 2003

Poison Pill Adoptions Fall To Ten-Year Low

New York (January 22, 2004) – U.S. public companies caught in the whirlwind of scandals and

eroding investor confidence responded to shareholder pressure and made themselves more

shareholder friendly by reducing their protection from hostile takeovers in 2003. According to

data compiled by TrueCours e, Inc., a New York-based research firm, hostile takeover defense

protection decreased significantly in 2003. “It appears that to some companies the threat of angry

investors exceeds the threat of potential raiders,” noted Jim Sussmann, president of TrueCourse.

TrueCourse measured relative takeover defense protection with its proprietary Bullet Proof Rating on a scale of 0 to 10, with 10 indicating the strongest takeover defenses. The average

takeover defense protection of companies in the S&P 500 fell 4.05% to 5.69 in 2003. The

average takeover defense protection of the Dow Industrials also declined 6.21% to 3.17, while

the average Bullet Proof Rating of companies that completed IPOs in 2003 plummeted 31.8% to 3.36. The Bullet Proof Rating is a weighted index that takes into account provisions and

procedural items that contribute to defending against hostile takeovers.

Biggest Decreases in Takeover Defense Protection - S&P 500 Bullet Proof Bullet Proof

The decrease in 2003 was driven primarily by companies switching to annually elected boards

from staggered board elections – where each director commonly stands for election every three

years and elections are held for only one-third of the board in a given year. The proportion of

companies that went public in 2003 with a classified board fell to 49.3% from 82% in 2002. The

decrease was also impacted by companies redeeming shareholder rights plans or “poison pills” as

well as removing supermajority vote requirements for approving mergers.

Proportion Of S&P 500 With Defense Provisions In Place S&P 500 S&P 500 Defense Provision

Pfizer, Inc., which was the largest company with a poison pill in force, dramatically reduced

their structural defenses over the last two years. On October 10, the company announced they

would accelerate the expiration date of their shareholder rights plan to January 1, 2004 from

October 2007. In the press release announcing the Board's decision to eliminate the rights plan,

Pfizer stated the decision to end the provision moves them further into the vanguard of

progressive corporate governance reform, and the action is designed to comply with recognized

best practices of corporate governance. “With a market cap over $250 billion, Pfizer doesn’t face

significant risk from opportunistic raiders, so reducing their defenses will put them in line with

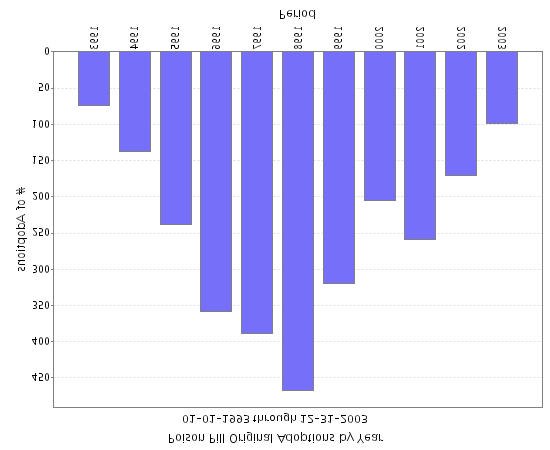

other mega caps,” said John Laide, vice president of TrueCourse. Poison Pill Adoptions

The rate of new adoptions of shareholder rights plans or poison pills fell to a ten-year low in

2003. Only 99 U.S. companies adopted new plans in 2003, down 42.11% from 2002 and the

lowest level since 74 plans were adopted back in 1993.

Proxy Proposals to Redeem or Require Vote on Poison Pills Joanne Allegra, vice president of TrueCourse, noted that, “there has been considerable pressure

on companies to comply with new best practices in corporate governance.” The number of

shareholder proposals to redeem or require a shareholder vote on poison pills continued to soar in

2003 with 100 proposals, up 194% since 2001 when only 34 proposals were made. “In many

cases, the issue is really a referendum on management and not really about poison pills at all -

almost a quarter (23%) of all companies that had a poison pill proxy proposal didn’t even have a

pill,” observed Allegra.

One company that bucked the trend and increased their takeover defenses in 2003 was Siebel Systems, Inc. In January, Siebel adopted a poison pill and increased their Bullet Proof Rating to

9.25 from 5.25. Siebel Systems is a rival of Oracle Corp, which launched a hostile bid for PeopleSoft on June 6, 2003. “If PeopleSoft had not prepared itself by adopting effective takeover

defenses, it’s unclear if Oracle would have significantly raised its original bid of $16 per share. At

this point, the raised bid means an extra $1.2 billion for PeopleSoft's shareholders if a deal is

comple ted,” said John Laide . “PeopleSoft vs. Oracle is a good example of the potential benefits

that shareholders and other constituencies such as customers and employees can derive from

takeover defenses,” added Laide . TrueCourse is a New York-based research firm specializing in takeover defense intelligence, proxy voting and corporate governance. TrueCourse provides online products, custom research and consulting services to institutional investors, leading investment banks and law firms. For more information on TrueCourse, visit www.SharkRepellent.net

CHECKLIST OF REQUIREMENTS FOR DRUG DISTRIBUTOR / MANUFACTURER; MEDICAL DEVICE; COSMETIC ESTABLISHMENTS General Requirements: (ALL FORMS TO BE ACCOMPLISHED IN TRIPLICATE) _________ Information as to activity of the establishment _________ Notarized Accomplished Petition Form / Joint Affidavit of Undertaking _________ Photocopy of Business Name Registration with DTI (if single proprietor); with SEC

Cas cliniques de réanimation - Exercices de révisionsInfirmier en unité de réanimation médico-chirurgicale. Votre vacation est de 8H00 à20H00. Vous avez en charge un secteur de trois box mais seuls deux sontMonsieur PAPO, âgé de 70 ans, a été admis le 29 juin 2006 pour prise en chargepost-opératoire d’un pontage aorto-bifémoral (pour anévrysme de l’aorte abdominale). - Insuff

TrueCourse, Inc.

TrueCourse, Inc.  Pfizer stated the decision to end the provision moves them further into the vanguard of

Pfizer stated the decision to end the provision moves them further into the vanguard of